The U.S. flood insurance market is entering a period of structural change.

For decades, the National Flood Insurance Program (NFIP) has served as the foundation of flood insurance in the United States, providing coverage for millions of property owners and helping communities recover from some of the nation’s most significant flood events. As flood risk evolves, new data, modeling capabilities, and private market participation are creating opportunities to strengthen the overall flood insurance ecosystem.

The question now is: what does a sustainable flood insurance market look like for the decades ahead?

That question was at the center of a recent Lloyd’s market discussion hosted by Ocean Ledger and KatRisk, where industry leaders explored the future of U.S. flood insurance, the evolving role of the private market, and the challenges of underwriting flood risk in a rapidly changing environment.

The conversation brought together perspectives spanning catastrophe modeling, regulation, underwriting, and reinsurance. While opinions differed on where the market is heading, there was broad agreement on one point: flood is no longer a niche peril or a government problem alone. It is becoming a central challenge for insurers, reinsurers, and capital providers globally.

Supporting a Changing Flood Risk Landscape

The NFIP was created in 1968 to address a market failure. Private insurers largely avoided flood risk because losses were difficult to model, highly correlated, and catastrophic when they occurred. The federal government stepped in to provide coverage and stabilize access to insurance in flood-prone communities.

For many years, the structure held.

For more than five decades, the NFIP has played a critical role in expanding access to flood insurance and establishing the foundation of the U.S. flood insurance market. The challenge today is not that the program failed to fulfill its purpose, but that the nature of flood risk and the value and complexity of the structures at risk have evolved significantly since the program’s creation.

Extreme precipitation events are becoming more frequent and severe. Urban development has expanded into vulnerable areas. Home values have increased, and critically, flood losses are occurring outside of traditionally mapped flood zones.

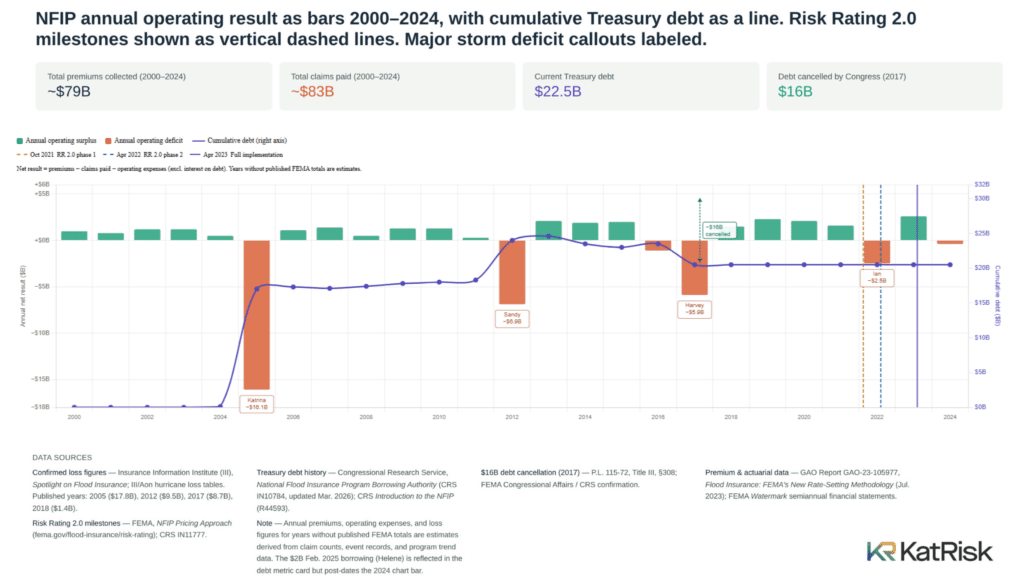

At the same time, the NFIP itself remains under significant financial strain. Following major catastrophe years including Hurricane Katrina, Superstorm Sandy, and Hurricane Harvey, the program accumulated substantial debt to the U.S. Treasury. Even after reforms introduced under Risk Rating 2.0, losses continue to outpace premium revenue.

That reality is driving a broader conversation about how public and private markets can work together to ensure long-term flood insurance availability, affordability, and resilience.

Risk Rating 2.0 Changed the Conversation, But Not Overnight

Risk Rating 2.0 represented one of the most significant overhauls in the history of the NFIP.

Its intent was straightforward: align premiums more closely with actual risk and reduce decades of cross-subsidization embedded within the program.

Historically, many policyholders paid rates that did not accurately reflect their exposure. In theory, a more actuarially sound pricing structure should improve market stability and create better conditions for private market participation.

The NFIP continues to rely on FEMA’s traditional Flood Insurance Rate Maps (FIRMs) to determine whether a property falls within a Special Flood Hazard Area and therefore requires flood insurance when backed by a federally regulated mortgage. Changing that framework would require Congressional action.

As a result, the program now operates with two complementary but distinct systems: flood maps used for regulatory and mandatory purchase purposes, and Risk Rating 2.0’s property-specific risk assessment methodology used for pricing. This reflects the reality that flood maps were originally designed as regulatory tools to identify areas of elevated risk, whereas Risk Rating 2.0 was developed to better reflect the unique characteristics and exposure of individual properties.

KatRisk has been a trusted partner to the NFIP since 2016, supporting FEMA’s efforts to better understand and quantify flood risk through advanced catastrophe modeling and analytics. The program’s evolution reflects years of collaboration across public and private stakeholders working toward a more risk-informed approach to flood insurance.

The challenge is that the transition is happening slowly.

Congressional caps limiting annual premium increases to 18% means that many properties will take years, potentially into the mid-2030s, to reach fully risk-based pricing.

That creates a difficult balancing act.

Premium increases are significant enough to push some policyholders out of the market, but not yet sufficient to fully close the program’s financial gap. Meanwhile, the underlying hazard itself continues to evolve.

The Private Market Opportunity Is Real, But So Are the Risks

One of the clearest themes from the discussion was that private market participation in flood is no longer theoretical.

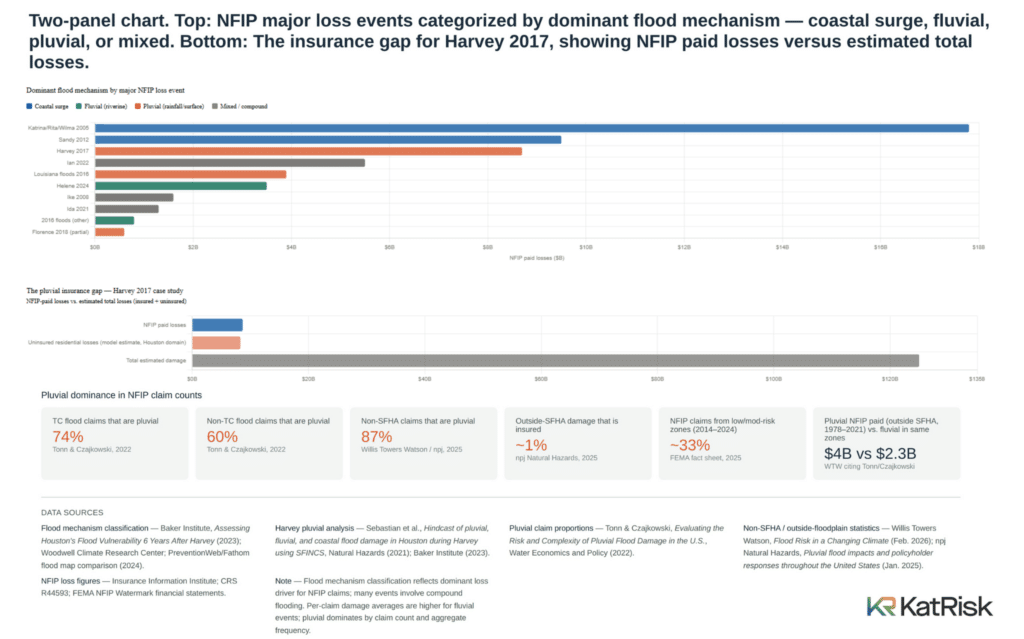

Insurers are increasingly underwriting risks outside Special Flood Hazard Areas (SFHAs), particularly where legacy flood maps or NFIP structures may not fully capture pluvial exposure.

That shift reflects a broader change in how the industry views flood risk.

Historically, flood underwriting focused heavily on fluvial and coastal flooding tied to rivers, storm surge, and mapped floodplains. But many of the most damaging recent events have highlighted the growing importance of pluvial flooding, intense rainfall overwhelming drainage systems and causing flooding well beyond designated flood zones.

Hurricane Harvey remains one of the clearest examples. While total economic losses exceeded $100 billion, a large portion of the damage occurred outside mandatory purchase zones, leaving significant uninsured losses behind.

For the private market, this creates a major opportunity.

Improved hazard data, higher-resolution modeling, and broader access to exposure analytics are making it increasingly possible to differentiate risk at a granular level. Insurers are no longer limited to broad flood zone assumptions.

But flood remains an unusually difficult peril.

Unlike many other catastrophe risks, flood is highly correlated, heavily influenced by local infrastructure and land use, and increasingly shaped by changing precipitation dynamics. That makes scaling a profitable flood portfolio far more complex than simply expanding underwriting appetite.

Several panelists raised concerns around adverse selection as well.

“As the market expands, the challenge is making sure we’re not simply redistributing risk, but actually improving how flood risk is understood and priced,” said Brandon Katz, EVP Strategy at KatRisk. “The industry has better tools, better data, and better science than ever before, but long-term market resilience depends on aligning underwriting confidence with the realities of evolving flood behavior.”

The question is not simply whether the private market can grow.

It is whether the market can grow in a way that remains resilient following major correlated loss events.

Flood Modeling Has Improved, But Confidence Still Matters

A significant portion of the discussion focused on modeling itself.

Flood models have evolved dramatically over the past decade. Higher-resolution terrain data, improved rainfall modeling, cloud computing, and more sophisticated event simulation capabilities are giving insurers a far more detailed understanding of flood behavior than was previously possible.

But confidence in the models remains central.

One challenge repeatedly raised was the industry’s reliance on NFIP claims data as a calibration benchmark. Because the NFIP has historically dominated the market, it remains one of the only large-scale flood claims datasets available in the U.S.

That creates a difficult dynamic.

If multiple vendors are calibrating toward the same underlying dataset, are models converging toward genuine physical accuracy, or simply converging toward the same historical biases?

The discussion also highlighted the limitations of relying too heavily on historical losses in a rapidly changing climate environment. Flood risk is not static. Urbanization, infrastructure changes, shifting precipitation patterns, and secondary impacts all influence how losses emerge over time. As a result, underwriters increasingly need models that capture not only historical patterns, but how flood behavior itself may evolve.

That does not mean abandoning historical validation.

It means combining empirical claims data with physically based modeling approaches capable of simulating how events originate, intensify, and translate into loss under changing conditions.

At KatRisk, flood modeling has focused heavily on combining physically based hazard science with high-resolution exposure analytics to better capture both fluvial and pluvial flood dynamics. This includes modeling how rainfall, terrain, land use, drainage infrastructure, and coastal interactions influence flood behavior at the property level, helping insurers move beyond broad flood zone assumptions toward a more detailed understanding of risk.

What a Sustainable Flood Market Could Look Like

Despite the complexity, the overall tone of the discussion was optimistic..

In many ways, the industry is more capable of underwriting flood risk today than at any point in its history.

“Translating technological advancements into an underwriting edge is not straightforward. MGAs that land and expand their niche, build in guardrails and invest in their own technical moats will be well positioned to unlock the opportunity, said Paige Roepers, CEO at Ocean Ledger.

Encouragingly, many of the building blocks are already in place. Advances in catastrophe modeling, improved data availability, and growing private market participation are creating new pathways to expand flood insurance capacity. Beyond traditional insurance and reinsurance, innovative structures such as parametric products, alternative capital, and insurance-linked securities (ILS) are beginning to play a larger role in how flood risk is financed.

Programs such as FEMA’s FloodSmart Re catastrophe bond have demonstrated that flood risk can be successfully transferred to the capital markets, providing additional capacity while diversifying sources of protection. As confidence in flood modeling continues to grow, there is an opportunity to build on that foundation with a broader and more active flood catastrophe bond market, helping attract new capital to support both public and private flood insurance solutions.

Ultimately building a sustainable market will require:

- Better alignment between pricing and actual risk

- Greater confidence in hazard and catastrophe modeling

- Continued investment in resilience and mitigation

- Long-term regulatory stability

- Reinsurance structures capable of supporting correlated catastrophe risk

- More transparent communication around exposure and uncertainty

Most importantly, it will require recognizing that flood risk is dynamic.

The market structures, underwriting approaches, and modeling assumptions that worked twenty years ago may not be sufficient for the next twenty. For example, Ocean Ledger is leveraging its ability to capture and predict localized coastal flood dynamics to design and launch a new insurance product catering to coastal businesses (hospitality, retail, large infrastructure).

The industry now has an opportunity to rethink how flood risk is understood, priced, and managed.

The question is whether the market can evolve quickly enough to meet the scale of the challenge.

----

This article was informed by discussions held during the “US Flood Policy at a Crossroads: Insurance, Reform & Resilience” event hosted by Ocean Ledger and KatRisk at Lloyd’s of London.